ABOUT FISG

Experience unparalleled stability, security, and efficiency in the Forex and CFD trading market.

Founded in Europe in 2011, InterStellar Group (FISG) is a top-tier brokerage with extensive experience in global financial markets. Through in-depth cooperation with international banks and the multi-dimensional construction of a global financial hub, FISG provides six major CFD products to global traders with a sustainable and robust trading ecosystem.

FISG's services cover four continents, with a total of more than 112,000 clients.

FISG-InterStellar Group boasts a sterling reputation worldwide and has been the recipient of many prestigious international accolades.

HOW SAFE ARE YOUR FUNDS WITH US?

We prioritize the safety and security of our clients' funds, as we understand how important it is to have peace of mind while investing. Here are some measures we take to ensure the safety of your funds:

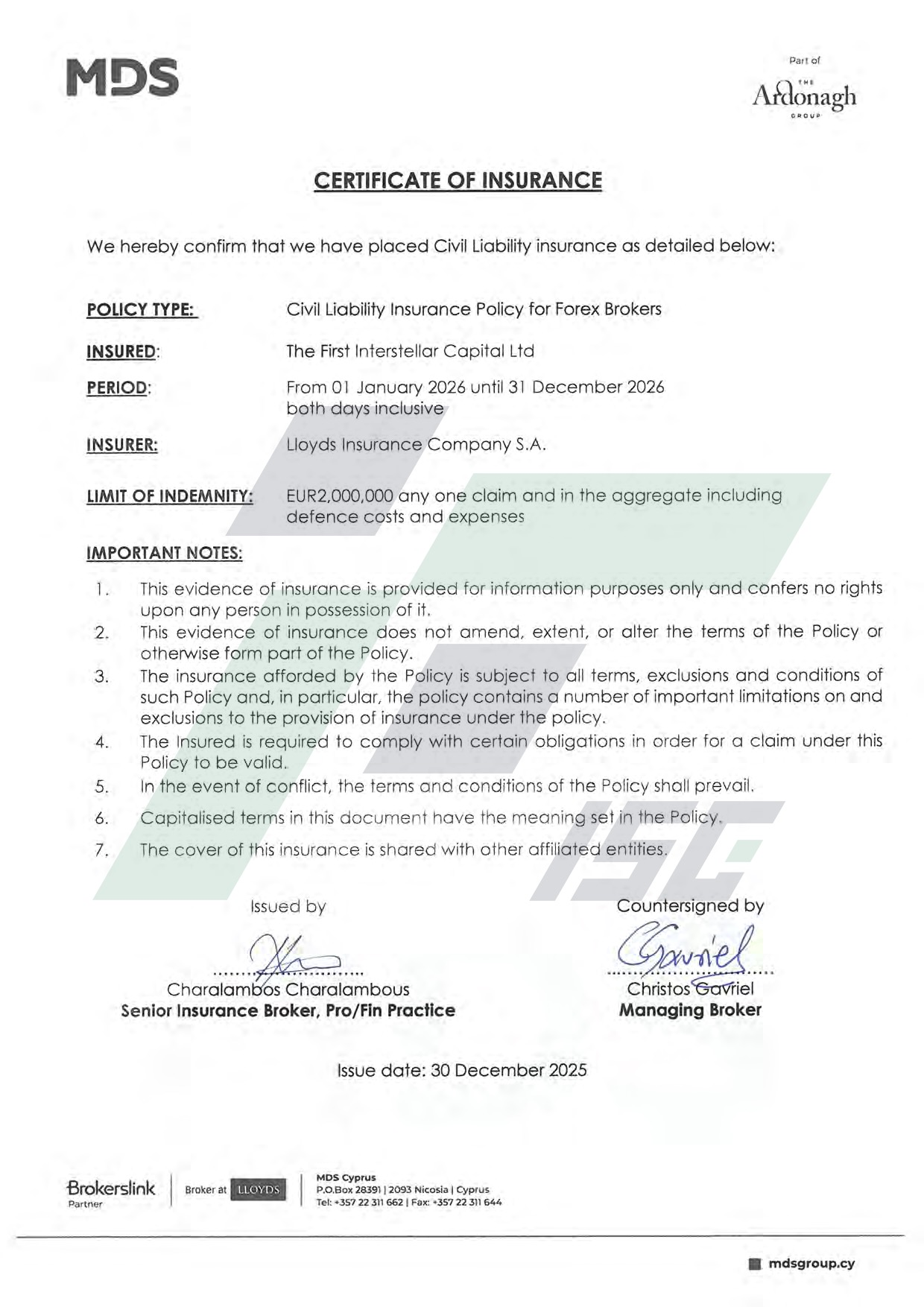

FUND INSURANCE

GENEROUS COVERAGE

We offer insurance compensation up to €2,000,000, ensuring the safety of your funds.

TRUSTED INSURER

Our policy is backed by Lloyd's of London, renowned for their reliability.

CLIENT PROTECTION

All clients under The First Interstellar Capital Ltd and First Interstellar Global Ltd are covered.

THE INVESTOR COMPENSATION FUND (ICF)

COMPREHENSIVE COVERAGE

Qualified applicants can receive a maximum compensation of €20,000.

REGULATED BY CYSEC

Ensuring smooth market operations and additional investor protections.

NEGATIVE BALANCE PROTECTION

Protects investors against negative balance incidents.

WHAT REGULATORY STANDARDS DO WE FOLLOW?

FISG is committed to maintaining high standards of regulatory compliance across its operations.

KYC Compliance

Identity verification and account security procedures

AML Measures

Controls designed to help prevent unlawful financial activity

Risk Control

Internal procedures that support operational integrity

Client Protection

Standards that promote transparency and accountability

Jurisdictional Compliance

Compliance practices aligned with applicable local frameworks

For full regulatory details, please refer to our Legal Compliance page.

MEET THE STARRY BUDDIES -

THE MASCOT OF FISG

- OAO

- AI Robot

OAO is an AI robot created by the First InterStellar Group, designed to accompany and support our InterStellar partners.

Inspired by an orbital observatory, its design embodies the combination of technology and exploration.

OAO loves learning and sharing knowledge, encouraging people to explore the market and future developments.

- DEXY

- THE AGILE INDEXER

DEXY represents the "index" in FISG products.

Its antenna features chip elements, symbolizing the rapid transmission of information.

Dexy is the liveliest and most agile member of the Starry Buddies.

- CRYPTA

- THE MYSTIC TRADER

Crypta represents "cryptocurrency" in FISG products.

Design inspired by ETH diamond structure with a transparent outer layer.

Crypta inspires exploration of new opportunities and technologies.

- ARGO

- THE METALLURGIC GUARDIAN

Argo represents "metal" in FISG products.

Its solid and steady design symbolizes stability and resilience in the market.

Argo serves as the reliable guardian of the Starry Buddies.

- STOCKTON

- THE MARKET MAESTRO

Stockton represents "stocks" in FISG products.

The lights around its neck shift in response to market conditions, reflecting price movements.

With clear logic and precise judgment, Stockton is the most rational member of the Starry Buddies.

- ENER

- THE SAGE OF ENERGY

Ener represents "energy" in FISG products.

Its fluid form and airflow convey the dynamic nature of the energy market.

As the oldest and wisest member, Ener embodies experience and foresight.

- KOIN

- THE FOREX VOYAGER

Koin represents "forex" in FISG products.

The head indicator instantly reflects currency changes, while the cape symbolizes free movement across global markets.

Koin adapts to dynamic market conditions, providing steady confidence and guidance.